Digital Lending Under Rbi's Framework: What Ai Can And Cannot Do

- 4 min read

Digital lending in India is a regulated environment where AI must operate within clear customer-protection and compliance boundaries.

RBI’s digital lending framework defines how regulated entities must manage digital credit journeys, including disbursement, repayment, disclosures, data handling, grievance redressal, and loan service provider relationships.

AI can add value in this environment, but only when it is designed inside the regulatory frame from the start.

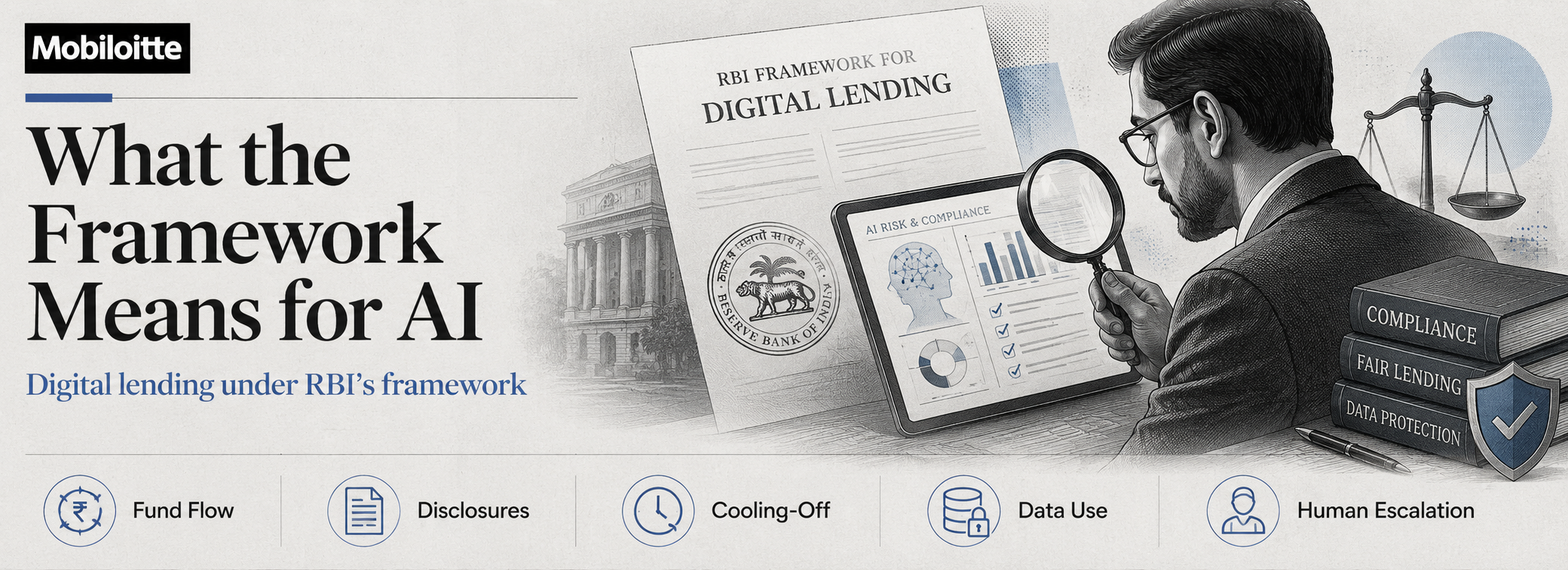

What the Framework Means for AI

1. Fund Flow Must Follow RBI Rules

Loan disbursement must happen directly from the regulated entity to the borrower’s bank account.

Repayments must also flow directly to the regulated entity.

AI workflows that support disbursement, repayment, or reconciliation must reflect this structure and cannot route funds through inappropriate third-party paths.

2. Required Disclosures Must Stay Clear

AI can personalize the borrower journey, but it cannot hide or weaken required disclosures.

The borrower must clearly receive key information such as loan terms, APR, charges, recovery mechanism, privacy policy, and grievance details.

Personalization should improve understanding, not obscure obligations.

3. Cooling-Off Rights Must Be Supported

Borrowers must be able to exit the loan during the cooling-off period as permitted under the framework.

AI-led servicing and customer journeys should clearly explain this right and support the workflow when borrowers choose to use it.

4. Data Use Must Be Purpose-Limited

AI in lending depends on data, but data use must follow consent, purpose limitation, minimization, and permitted retention rules.

This affects AI training, inference, personalization, fraud checks, and servicing automation.

The key question is:

Was this data collected and used for this purpose under the approved framework?

5. Grievance Escalation Must Remain Human-Accessible

AI chatbots and copilots can support borrower queries.

But complaints, disputes, and sensitive issues must escalate clearly to human grievance redressal channels.

AI should support redressal, not replace accountability.

What AI Can Do Well

Within RBI’s framework, AI can create strong value in:

- underwriting decision support

- document and identity verification

- fraud screening

- borrower communication

- vernacular customer support

- EMI and servicing queries

- collections support with proper controls

- operator assistance for regulated workflows

The strongest use of AI is not uncontrolled automation.

It is explainable, auditable decision support.

Where AI Projects Get Into Trouble

AI-led lending projects usually fail when they:

- design fund flows outside the regulated structure

- personalize journeys in ways that hide required disclosures

- use customer data without clear consent or purpose

- treat LSPs as a way to shift responsibility away from the regulated entity

- automate sensitive decisions without explainability or review

These are not small UX issues.

They are compliance and architecture risks.

What Strong Programs Do

Strong AI lending programs treat RBI’s framework as a design input.

They build around:

- regulated fund flow

- transparent disclosures

- consent and data minimization

- explainable underwriting

- audit trails

- human escalation

- grievance redressal

- compliance involvement during the build

This makes AI easier to trust, audit, and scale.

Conclusion

AI can improve digital lending in India, but it cannot bypass the regulatory frame.

It can support underwriting, verification, fraud detection, servicing, communication, and operational efficiency.

But it must respect borrower protections, regulated entity accountability, data boundaries, disclosures, grievance rights, and DLG rules.

The strongest question is not:

How far can AI go?

It is:

How can AI create value safely inside the RBI framework?

FAQs

1.Can AI be used in digital lending in India?

Yes. AI can support underwriting, verification, fraud detection, servicing, and customer communication when designed within RBI’s framework.

2.What is the biggest AI risk in digital lending?

The biggest risk is designing AI workflows that ignore fund flow rules, disclosures, consent, grievance escalation, or regulated entity responsibility.

3.Can AI personalize borrower journeys?

Yes, but required disclosures must remain clear and visible.

4.Can an LSP take over the regulated entity’s obligations?

No. The regulated entity remains accountable for compliance and borrower protection.

5.What is the safest way to build AI in digital lending?

Build AI with clear consent, audit trails, explainability, human escalation, compliant fund flow, and compliance review from the start.