Account Aggregator And Uli: Ai On India's Emerging Credit Infrastructure

- 4 min read

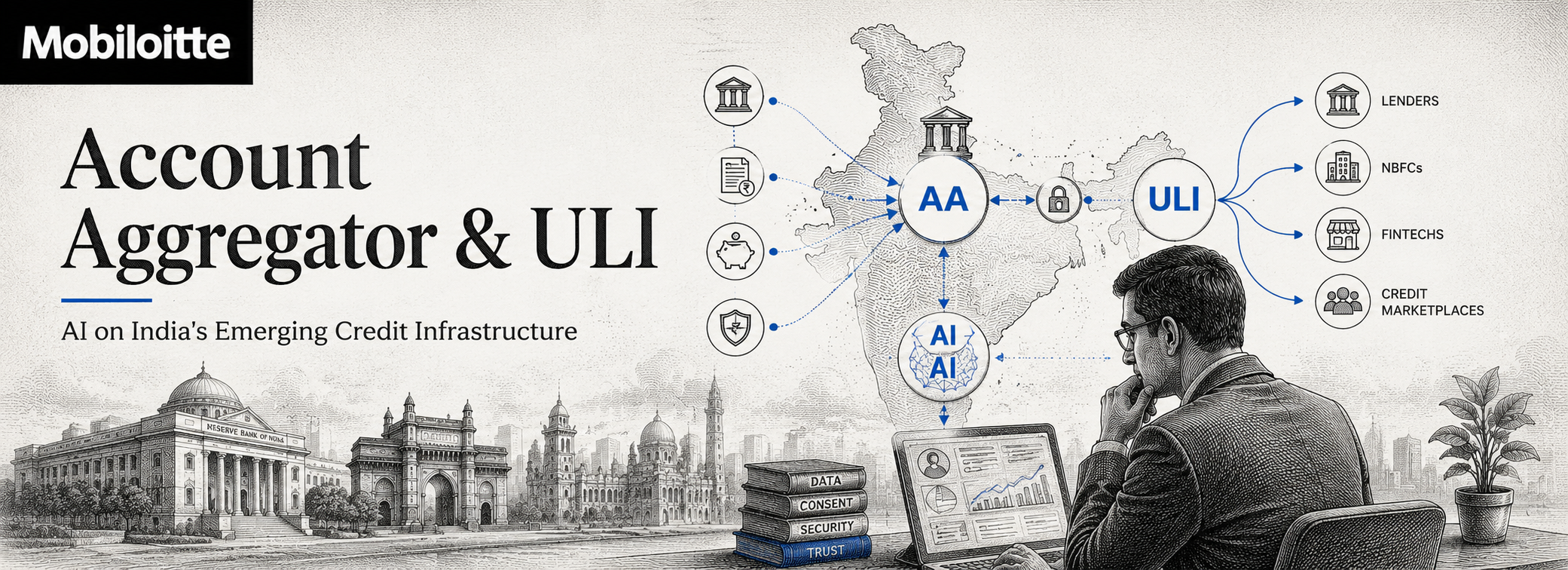

India is building a powerful digital credit infrastructure.

The Account Aggregator framework enables consent-based financial data sharing between regulated entities. The Unified Lending Interface (ULI) is emerging as a common digital rail for faster, more interoperable lending journeys.

For banks and NBFCs, this changes how AI should be designed.

AI that uses these rails can work with cleaner, more current, consent-backed data. AI that ignores them ends up recreating work the infrastructure is already solving.

What Account Aggregator Enables

Account Aggregators connect Financial Information Providers and Financial Information Users through customer consent.

For lending AI, this creates major advantages.

Structured Underwriting Data

Lenders can access structured financial data instead of relying only on uploaded PDFs, manual bank statements, or scraping.

This improves speed, accuracy, and auditability.

Better Financial Visibility

With consent, lenders can understand more of the borrower’s financial picture.

This helps underwriting, risk monitoring, servicing, collections, and customer segmentation.

Clear Consent Trail

AA creates a record of who gave consent, for what data, for what purpose, and for how long.

That gives compliance and audit teams stronger evidence.

Better Customer Experience

Borrowers no longer need to repeatedly upload documents or chase bank statements.

The journey becomes faster and cleaner.

What ULI Is Shaping Toward

ULI is still maturing, but the direction is clear.

It aims to create a standardized digital infrastructure for lending, helping lenders access data and orchestrate credit journeys through common rails.

For AI, this matters because it reduces integration friction and makes lending workflows faster.

Instead of building many custom integrations, lenders can design around more standardized data flows.

How AI Should Be Designed for These Rails

Treat AA and ULI as Core Infrastructure

Underwriting, risk monitoring, servicing, and customer intelligence should treat structured consent-backed data as a primary source.

Legacy document uploads can remain fallback paths, but they should not define the future model.

Respect Consent and Purpose

AA and ULI data must be used only for the purpose the customer approved.

Reuse outside that consent is not innovation.

It is a governance risk.

Build for Evolution

AA coverage is expanding, and ULI is still developing.

AI architecture should be flexible enough to absorb new data sources, consent flows, APIs, and lending use cases.

What Is Still Hard

AA and ULI are strong infrastructure rails, but they are not silver bullets.

Coverage can vary. Customer consent literacy may differ. Edge cases such as joint accounts, NRI accounts, recent activity, or incomplete records still need handling.

Mature AI programs account for these gaps with fallback logic, exception handling, and governance controls.

What This Changes

Earlier, AI-led lending often depended on uploaded PDFs, scraped data, bureau pulls, and fragmented integrations.

Now, lenders can increasingly build around structured, consent-based, interoperable financial data.

That improves underwriting, fraud detection, risk monitoring, servicing, and customer intelligence.

The opportunity is clear:

Lenders that use AA and ULI well can build faster, cleaner, and more auditable AI-led credit journeys.

Conclusion

Account Aggregator and ULI are changing the foundation of AI-led lending in India.

AA enables structured, consent-backed financial data.

ULI is shaping a more standardized lending infrastructure.

Together, they make AI in credit more practical, auditable, and scalable.

The strongest lenders will not treat these rails as optional integrations.

They will design AI around them from the start.

FAQs

1.What is Account Aggregator?

Account Aggregator is a consent-based framework that allows financial data to be shared securely between regulated entities.

2.What is ULI?

ULI is an emerging digital lending infrastructure designed to standardize and simplify credit journeys.

3.How does AA help AI underwriting?

It gives lenders structured, consent-backed financial data, reducing dependence on manual uploads and document parsing.

4.Can AI reuse AA data for any purpose?

No. AI must respect consent, purpose limitation, and data governance rules.

5.What is the biggest design mistake?

Treating AA and ULI as optional integrations instead of core infrastructure for AI-led lending.