Transforming Insurance Through Real-time Decisioning And Predictive Risk Intelligence

- 10 min read

Insurance leaders envision a future where claims are settled in minutes, underwriting decisions are instantly accurate and customer interactions are intelligent, proactive and seamless. This vision is not just aspirational; it is necessary for insurers competing in a digital-first landscape defined by rising customer expectations, increasing fraud complexity and cost pressure across operations.

Yet the reality of most insurance operational systems paints a different picture. Claims are delayed due to manual reviews. Underwriting workflows are fragmented across tools. Adjusters struggle with limited visibility. Data sits in silos, making risk assessment slow and inconsistent. Talent shortages create operational backlogs. Fraud is becoming more sophisticated, outpacing rule-based detection systems.

The gap between vision and execution is widening. To close it, insurers must shift from manual, document-heavy processes to real-time, AI-powered decision systems. Mobiloitte helps insurers build scalable, secure and intelligent platforms that drive automation in claims, underwriting and risk scoring. With AI orchestrating workflows and data, insurers gain precision, speed and operational resilience.

Why Insurance Must Move Toward Real-Time AI Decisioning

Several forces are reshaping the insurance landscape.

Rising Customer Expectations

Policyholders expect faster claims processing, transparent communication and personalized experiences across digital channels.

Increased Claims Volume and Complexity

Natural disasters, health events and cyber incidents have made claims more frequent and unpredictable.

Fraud Evolution

Insurance fraud networks use digital channels, synthetic identities and sophisticated document manipulation techniques.

Regulatory Pressure

Insurers must demonstrate fairness, accuracy, auditability and transparency in their claims and underwriting decisions.

Operational Inefficiencies

Manual workflows, paper-based processes and legacy core systems create delays and increase administrative costs.

Data Explosion

Telematics, IoT devices, digital medical records, property imagery and behavioral datasets provide rich insight, but require AI to process efficiently.

AI-powered claims automation and intelligent underwriting enable insurers to manage these forces at scale, reducing turnaround times and improving decision quality.

Why Traditional Claims and Underwriting Systems Are Falling BehindLegacy systems and manual processes hold insurers back in several critical ways.

Fragmented Workflows

Claims move across multiple departments and tools, leading to delays, duplication and poor case visibility.

Static Rule-Based Decisions

Rules cannot adapt to new risks or fraud behaviors. They require constant manual updates.

High Operational Costs

Adjusters and underwriters spend excessive time on data collection and document review instead of decision making.

Limited Fraud Detection

Manual checks cannot detect sophisticated fraud patterns that evolve quickly.

Slow Underwriting Processes

Underwriters spend hours reviewing historical data, verifying documents and assessing risk manually.

Lack of Predictive Insights

Traditional systems react to events after they occur instead of anticipating outcomes.

AI addresses these gaps with adaptive models, continuous learning and automated workflows.

How AI Transforms Claims Automation and Underwriting

AI introduces intelligence, speed and accuracy into insurance operations.

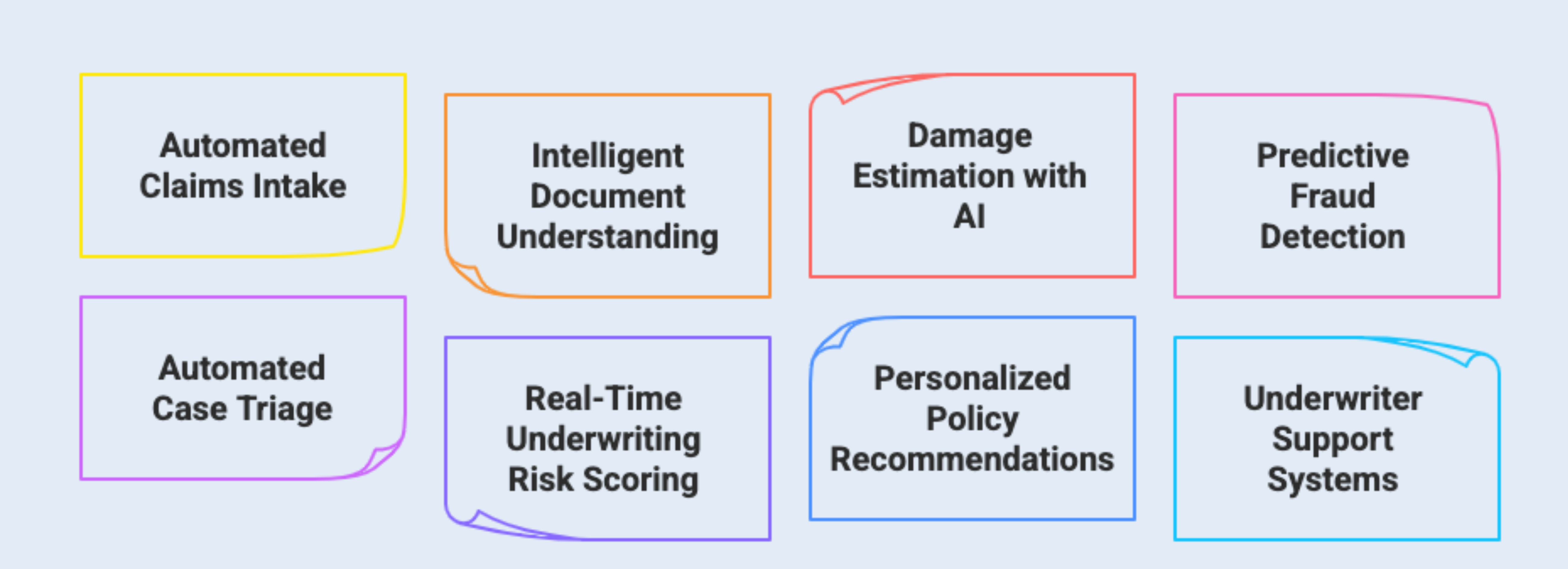

Automated Claims Intake

AI extracts data from documents, emails, voice notes and images, reducing manual entry.

Intelligent Document Understanding

Computer vision interprets medical reports, invoices, repair images and assessment documents.

Damage Estimation with AI

Image recognition models estimate property or vehicle damage instantly.

Predictive Fraud Detection

ML models analyze cross-claim behavior, identity patterns and historical risk indicators to flag fraud in real time.

Automated Case Triage

AI assigns claims to the right adjusters based on complexity, risk level and skill requirements.

Real-Time Underwriting Risk Scoring

Predictive models evaluate applicant risk using behavioral, historical and alternative datasets.

Personalized Policy Recommendations

AI suggests coverage tailored to individual needs and risk profiles.

Underwriter Support Systems

AI provides insights, highlights anomalies and recommends actions to help underwriters make accurate decisions.

Platforms like Converiqo.ai help automate case routing, alerts and compliance workflows. Mobiloitte builds the AI and platform engine that powers decision intelligence across the insurance lifecycle.

High-Impact Use Cases Transforming Insurance Operations

Instant Claims Pre-Assessment

AI reviews claim submissions, validates documents and pre-screens cases within seconds.

Property Damage Estimation

For home or auto claims, AI models analyze images to estimate repair costs.

Health Claims Automation

AI extracts medical codes, validates procedures and accelerates approvals.

Fraud Detection

AI identifies suspicious behavioral and relational patterns across policies.

Predictive Underwriting

AI scores applicants using a combination of historical, demographic and behavioral data.

Risk-Based Pricing

Policies are priced dynamically based on predicted risk and loss likelihood.

Customer Service Automation

AI chat interfaces support claimants and policyholders with instant updates.

Workflow Automation

Converiqo.ai integrates these intelligence layers into automated, trackable, compliant workflows.

These use cases improve customer satisfaction, reduce claim cycle time and increase operational efficiency.

Strategic Framework for Deploying AI Across Claims and Underwriting

Phase 1: Define Value Priorities

Determine which part of the claims or underwriting lifecycle offers the highest ROI.

Phase 2: Build a Unified Data Foundation

AI models require consistent, well-structured data across claims history, policy systems, documents and images.

Phase 3: Deploy Core AI Models

Models include fraud detection, document understanding, damage estimation, triage scoring and risk prediction.

Phase 4: Integrate Workflow Automation Tools

Platforms like Converiqo.ai handle routing, notifications, compliance flags and escalation paths.

Phase 5: Train Claims Adjusters and Underwriters

Teams need digital fluency to interpret AI recommendations. GyanBatua.ai helps insurers upskill their workforce.

Phase 6: Implement Continuous Monitoring

Models require periodic evaluation to ensure fairness, accuracy and regulatory compliance.

Phase 7: Scale Across Product Lines

Start with auto or health, then expand to property, life and specialty insurance.

This structured approach reduces implementation risk and accelerates time to value.

Organizational Readiness for AI-Driven Insurance Operations

Insurers must prepare across three dimensions:

Technology

A modernized system architecture that supports API integrations, cloud deployment and secure data pipelines.

Process

Standardized workflows for claims intake, underwriting evaluation and fraud reviews.

People

A workforce ready to leverage AI insights. Underwriters and adjusters must collaborate with intelligent systems instead of working around them.

Mobiloitte supports insurers in readiness assessments, helping them identify capability gaps before implementation.

Key Challenges and How to Address Them

Limited Data Quality

Invest in structured data pipelines and ongoing cleansing.

Regulatory Scrutiny

Ensure transparency in decision-making and audit readiness.

Model Bias

Continuously monitor for fairness and recalibrate models accordingly.

Change Resistance

Train teams early to build trust and encourage adoption.

Integration Complexity

Modular deployment and API-driven architecture minimize disruption.

Challenges become manageable with a phased transformation roadmap.

Why AI Claims Automation and Intelligent Underwriting Are Now Strategic Imperatives

The insurer of the future operates with real-time intelligence, automated decisions and enhanced human oversight.

AI provides clear competitive advantages:

- Faster claims settlement

- Improved fraud prevention

- Higher customer satisfaction

- Increased underwriting accuracy

- Reduced operational cost

- Stronger risk management

- Better regulatory preparedness

- Scalable automation models

Insurers that adopt AI early will shape industry standards. Those who delay risk higher losses, slower operations and reduced market relevance.

10. Frequently Asked Questions

1.How does AI speed up claims processing?

AI automates document extraction, damage assessment and triage.

2.Can AI detect insurance fraud?

Yes. AI identifies suspicious patterns that manual reviews miss.

3.Does AI replace claims adjusters?

No. It enhances their decision-making by reducing their manual workload.

4.How does AI support underwriting?

AI evaluates risk using historical, behavioral and external data.

5.What datasets are needed for AI underwriting?

Claims history, applicant profiles, property data and behavioral metrics.

6.Can AI improve customer satisfaction?

Yes. Faster claims and transparent communication significantly improve experience.

7.Is AI secure in insurance?

With proper governance, AI increases data security and compliance.

8.Does AI reduce operational cost?

Automation lowers manual processing time and resource needs.

9.Can AI help with regulatory compliance?

Yes. AI creates auditable processes and documentation.

10/How does AI identify fraudulent medical claims?

By analyzing coding patterns, inconsistencies and unusual billing behaviors.

11.What are the risks of using AI in insurance?

Bias, data errors, poor integration and lack of transparency.

12.How long does AI implementation take?

A phased rollout can begin delivering results in a few months.

To Know More Contact Us : https://www.mobiloitte.com/contact-us